The Importance of Asset Progression Planning

Are you planning to upgrade your house, but worried about managing your cashflow? As you grow older, you may have different priorities and goals. Asset progression planning is crucial to ensure that you are able to achieve your retirement goals, while having a good amount of cash and reserve funds.

Why You Should Start Your Property Asset Progression

The most valuable asset that you own now is probably your HDB flat. With adequate planning that aims to upgrade your property assets, you can utilise this to your benefit to grow your wealth and ensure a comfortable retirement. This simple guide will show you why you should start your property asset progression now.

#1 – Your HDB Home Is Not An Investment

You might think that your HDB home is an investment, but is that really so? The mission of the Housing Development Board is to provide affordable homes of quality and value.* What this means is that your HDB home will always be anchored to a value to ensure it remains at an affordable price point, and your capital gains will always be limited by government policies.

If you’re counting on the Selective En Bloc Redevelopment Scheme (SERS) to leverage on the ‘en-bloc’ potential of your home, you might be waiting in vain. Only about 5% of all HDB flats in Singapore* are eligible for SERS, while the remaining 95% of HDB homeowners will have to pay to return their flat to the government.

Just by considering these stringent government policies, you can already see that the capital gains of your HDB flat are heavily limited. You may think of your HDB as a home, but never consider it as an investment.

#2 – Your HDB Loan and CPF Accrued Interest Is Snowballing

Let’s take for example, that you purchased a $360,000 resale flat. You would have paid:

10% downpayment = $36,000

Stamp duty = $5,400

Mortgage duty = $500

Legal fees = $2,000

Total CPF used for initial payment = $43,900

Instalment for 25 years = $1,202/month or $14,424/year

Over time, if we continue paying for our flats until the end of the loan tenure of 25 years, we would have used $688,000 from our CPF OA account, and will have to refund it when we sell our property. Out of this amount, close to $95,667.26 will be accrued interest! Our initial plan to buy a property worth $360,000 has now ballooned to $688,000.

Don’t let this loan and interest continue growing. Selling your HDB flat means letting go of this loan that can snowball to a huge amount over time.

#3 – The Value Of Your HDB Is Decreasing Every Day

As your HDB flat depreciates over time, the value of the flat eventually becomes ZERO.

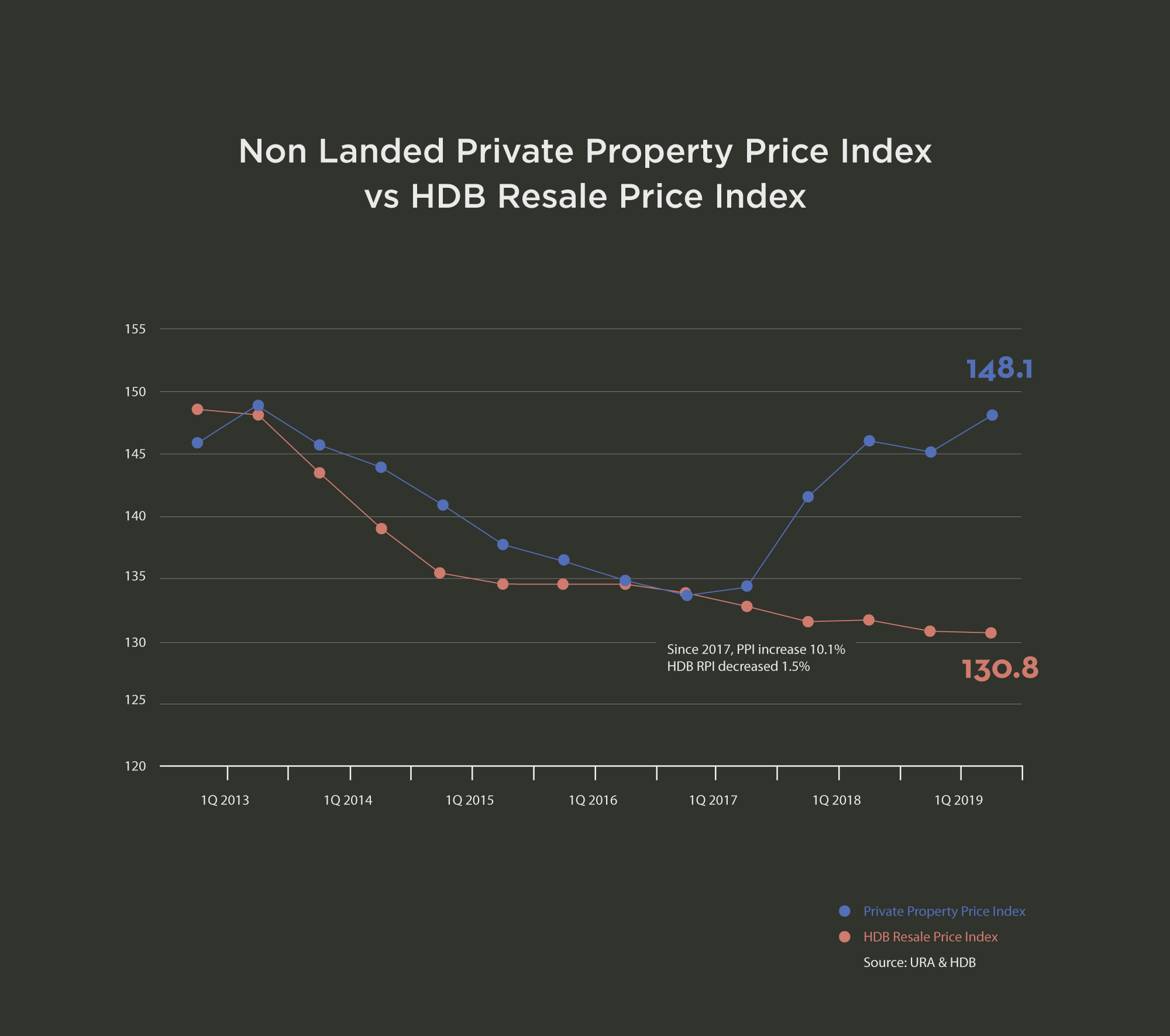

Don’t just take my word for it, the resale prices of HDB flats speak for themselves. Since its peak in 2013, HDB resale prices have been on a downward trend for more than 6 years, depreciating at a rate of 2.1% per year. The longer you stay in your HDB home, the more capital you are losing.

Since 2013, major policy changes have resulted in the drop of HDB prices.* As seen from the charts, the effect of this is still being seen today.

While your most valuable asset now may be your HDB flat, this will no longer be true in a couple of years time. Make your move early to get your first mover advantage.

*Policy Changes:

-ABSD 5% imposes in PRs purchasing HDB.

-MAS will cap the MSR at 30% of borrowers gross monthly income.

-Reduce maximum loan tenure from 30 to 25 years.

Options for HDB Owners

Do Nothing

Continue staying in your current HDB home comfortably and forego your opportunity for asset progression

Keep your HDB and buy a new condo

Continue staying in your current HDB home and earn a passive income from your condo

Sell your HDB and buy a new condo

Upgrade your lifestyle and maximising the value of your property asset

HDB vs Private

What are the prospects of Private Property prices?

With an increasing supply of new HDB flats and the continual rise of prices of private properties, it is expected that the difference between the two types of assets is likely to widen - with HDB resale prices continuing to decline.

Now, let’s have a look at what some of the leading banks in singapore has to say about the property market.

It anticipated a larger number of single-person households would drive home sales.

This means a compound annual growth rate of 1.5% to 3.2% over the next 12 years as growth in homeowners' incomes "keep pace" with the rise in private-property prices.

Case Study

Max and Christina, aged 40 and 36 with a combined income of $12,000.

Initial Plan:

– Sell their 4rm HDB flat and buy a Resale 5rm HDB.

After a planning session with me:

– They upgraded to a 3 Bedroom Condominium without using any of their savings;

– Maintained a CASH reserve of $100,000;

– en route to their second property in the coming years.

"Aiya..."

I would like to end by sharing some of the common regrets from clients that I've met. It is my sincere hope that you can be well informed and make the right decisions henceforth.

--------------------------------------------------

During our sharing session, I will share with you:

- An in-depth financial calculation process to allow you to understand your cash proceeds, cash outlay etc.

_____

- The 3 ways to analyse the available options in the property market and determine the most profitable yet undervalued property choices that are AFFORDABLE for you.

_____

- The TOP 5 questions you MUST ask before buying any property.

______

- A detailed assessment to determine if you should keep or sell your existing property.

Coffee?

Every household is unique, and I would love to provide you with a suitable strategy that is specific to your profile and goals. Contact me at 9234 5266 for a free sharing session with no obligations at any time.

______________________________________________________________

Source:

*https://www.hdb.gov.sg/cs/infoweb/about-us/vision-mission-and-values/vision-and-mission

*https://www.channelnewsasia.com/news/singapore/ndr-2018-scheme-planned-to-redevelop-more-old-hdb-flats-before-10631458

Contact

229 Mountbatten Rd,

Singapore 398007

Phone: +65 9234 5266

Email: yongpengyeo@gmail.com

Facebook: Yongpengproperty

Instagram: Yongpengproperty

Subscribe

Get access to latest news and all the new launches by subcribing here.

Copyright ©Yongpengproperty 2020 | Privacy Policy

ERA Realty Network Pte Ltd. (CEA Licence No. L3002382K) | CEA Reg No. R062132G

Disclaimer: The information is subject to change as may be required. All information provided have been treated with care and developer and/or marketing agent should not be liable for any inaccuracy.